This post is about mindset, culture, implicit assumptions. The big assumption in neoclassical economics is ergodicity, or equilibrium, or stationarity, or stability — basically the idea that nothing ever changes fundamentally. Things may fluctuate but they always return to some state of normality. Naively, that doesn’t fit with the idea of a growing economy, innovation, and change. So something’s up. I’ll explore what that is by replacing the mental image of stability with something that doesn’t return to normality: a nuclear explosion.

E pluribus unum — micro to macro

Equilibrium thinking in economics has clearly traceable historical roots. Chapter 1 of Eric Beinhocker’s book is a wonderful summary of where it comes from. In short: it comes from equilibrium thermodynamics — the study of gases, liquids, solids, under conditions where everything is allowed to come to rest. This field developed in the 19th century when people were interested in steam engines. In other words, it was all about gases in boxes (steam in cylinders).

Social researchers of the 19th century were impressed by the success of this branch of science, and also by its similarity to economics. A gas is a macroscopic thing, characterized by macroscopic properties — temperature, pressure, volume. But it consists of many microscopic constituents (molecules) whose interactions collectively create the macroscopic state. The study of macroscopic properties arising from microscopic interactions is called statistical mechanics. That really does sound like economics: an economy is a macroscopic thing, characterized by macroscopic properties such as GDP and trade balances, and those macroscopic properties arise from myriad microscopic constituents (people) interacting with each other.

So far so good. I completely agree with the analogy at this level: economics really is about a lot of microscopic constituents generating macroscopic behavior. But… what was done in 19th-century thermodynamics and statistical mechanics was based on the assumption that things are well described as being in equilibrium. That is not the case in economics (we have growth), and a lot of equilibrium intuition simply doesn’t apply. More precisely, if there are quantities in economics that are sensibly described as being in equilibrium, then they will have to be carefully constructed — they’re secondary properties of the process, not the process itself.

Time and a non-field

This doesn’t invalidate the analogy between statistical mechanics and economics, it just says that we have to look at non-equilibrium statistical mechanics to learn from the analogy. So what do we have there? Non-equilibrium statistical mechanics is a much more varied field (this is always true for “non”-fields — by definition, they are anything but something specific). Also, the usual caveats apply: we’re doing science, not magic, which means we’re building a model that will capture some aspects of reality and give meaningful answers in a limited range of situations. Outside that range it will be invalid.

The big difference between equilibrium and non-equilibrium is the role played by time. In equilibrium, everything is allowed to come to rest, that means time is allowed to play out till the end before the system is studied. We set things up, then (mathematically) wait an infinitely long time, and then look where we’ve got to. Non-equilibrium statistical mechanics doesn’t do that. It doesn’t just look at the end state but at the transition to that end state — even more radical: it doesn’t assume that an end-state exists. In other words, it studies dynamics, it studies what happens as time passes (not where we get to at the end of time). Of course there are far more ways to get from A to B than there are As and Bs. The study of dynamics is more varied than the study of the end points of dynamics.

Capitalism

Now — what about that nuclear explosion? It’s a process that is not in equilibrium at all, and it was very important in the 20th century. In such an explosion, atomic nuclei break up. In doing so they release neutrons, and those neutrons can cause other nuclei to break up and release more neutrons that cause other nuclei to break up etc. — the famous nuclear chain reaction.

One important question is how many additional neutrons are set free due to the setting free of one neutron (averaged over all neutrons of one generation). If the number is greater than one, then we have a super-critical run-away solution. Something is producing more of itself. The process is fundamentally noisy, and it’s fundamentally multiplicative. The number of neutrons follows noisy exponential growth.

What else can generate more of itself? Capital. The genius of capitalism is to allow excess resources to be used to create more of themselves. Sometimes that works, sometimes it fails — the process is both noisy and multiplicative.

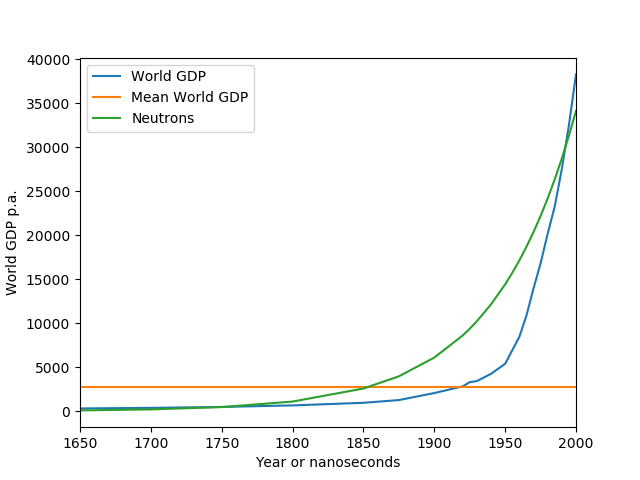

Let’s look at some data, and plot annual global GDP. For comparison, let’s plot its average (time-averaged over the plotted period) — if GDP was an equilibrium process it should hover around that value. For a nuclear explosion we could plot the number of free neutrons as a function of time. I don’t have data for this (direct measurement is a bit tricky, and detailed models are fairly confidential), but for a few hundred nanoseconds it will be exponential growth, so I’ll just plot exponential growth.

There are some differences between world GDP and exponential growth, but we’re definitely dealing with something that’s closer to a nuclear explosion (green line) than to an equilibrium process (yellow line). Of course the time scales are different, but economic growth and a nuclear explosion are similar.

When we model an explosion, we’re modeling a non-equilibrium process. Everything is flying apart, and naively there’s nothing stable about it. But there’s regularity even as things do fly apart — for example, for some limited time (while the chain reaction is running) each neutron sets free a more or less stable (certainly random!) number of new neutrons. We have to dig into the mechanics of the system to find something stable. Not impossible, but not trivial either.

Every economist knows that multiplicative growth is the null model not only for the nuclear explosion but also for the economy (GDP, asset prices etc). Nevertheless, the neoclassical economics mindset is one of equilibrium. That’s because some secondary properties of economic growth are quite stable (e.g. the exponential GDP growth rate), but equilibrium should not be our mindset. When we think about economics we should have the image of a slow nuclear explosion in mind. That’s very very different from the image of a gas in a box in equilibrium. The current formalism thinks: gas in a box in equilibrium. We think: explosion. Consequently, we will ask different questions and come to different conclusions about what we’re doing on planet Earth.

___________________________________________________________________________________________________

Curious about Ergodicity Economics?

Join our mailing list.

Seriously curious?

Get the textbook.

Pingback: Winner take all – Ergodicity Economics

Pingback: Winner take all – Ergodicity Economics

A great read thanks for sharing. I look forward to your next post

A great read thanks for sharing. I look forward to your next post

This is essentially how I understand things. The macroeconomy is dominated by positive feedback (driving exponential growth), but the microeconomy is dominated by negative feedback (which is equilibrating). The thing is that equilibrium isn’t a good model because the agents–humans–aren’t at equilibrium (if we were, we’d be dead). But we are satisficing. That is, we can be temporarily satisfied, and thus cease acting. If enough people do that, we will end up with a given price at a given time in a given place that will clear–supply will equal demand. Do something silly like add in time and space, and all of a sudden, you end up with a rugged landscape of prices.

What this suggests, though, is that the economy is in fact driven by bipolar feedback. There is positive feedback dominating at the macro-level and negative feedback dominating at the micro-level, with the result that positive and negative feedback are occurring simultaneously. This causes leaps into new phase spaces, which is the definition of creativity.

It also depends on how we understand “the economy.” There is the catallaxy, which is the system of mutually beneficial trade; there is money/finance, which is its own system and is obviously heavily influential on the catallaxy; and there is technological innovation, which is what drives most economic growth. Government regulations necessarily have an effect, mostly an equilibrating effect; government spending is a mixed bag that probably cancels itself out. Wars necessarily destroy wealth (but, because of the way GDP is calculated, will also increase GDP). All of these factors have to be taken into consideration when understanding what is happening in any given economy at any given time and place.

There are some economists–Ludwig Lacchman, Peter Lewin, and some other Austrian economists influenced by Lacchman–who are already on board with the idea of the disequilibrium economy. I’m more partial to the idea of the far-from-equilibrium economy, in which paradoxical relations drive creativity and thus increase wealth over time. It looks like that’s where you’re heading, more or less.

This is essentially how I understand things. The macroeconomy is dominated by positive feedback (driving exponential growth), but the microeconomy is dominated by negative feedback (which is equilibrating). The thing is that equilibrium isn’t a good model because the agents–humans–aren’t at equilibrium (if we were, we’d be dead). But we are satisficing. That is, we can be temporarily satisfied, and thus cease acting. If enough people do that, we will end up with a given price at a given time in a given place that will clear–supply will equal demand. Do something silly like add in time and space, and all of a sudden, you end up with a rugged landscape of prices.

What this suggests, though, is that the economy is in fact driven by bipolar feedback. There is positive feedback dominating at the macro-level and negative feedback dominating at the micro-level, with the result that positive and negative feedback are occurring simultaneously. This causes leaps into new phase spaces, which is the definition of creativity.

It also depends on how we understand “the economy.” There is the catallaxy, which is the system of mutually beneficial trade; there is money/finance, which is its own system and is obviously heavily influential on the catallaxy; and there is technological innovation, which is what drives most economic growth. Government regulations necessarily have an effect, mostly an equilibrating effect; government spending is a mixed bag that probably cancels itself out. Wars necessarily destroy wealth (but, because of the way GDP is calculated, will also increase GDP). All of these factors have to be taken into consideration when understanding what is happening in any given economy at any given time and place.

There are some economists–Ludwig Lacchman, Peter Lewin, and some other Austrian economists influenced by Lacchman–who are already on board with the idea of the disequilibrium economy. I’m more partial to the idea of the far-from-equilibrium economy, in which paradoxical relations drive creativity and thus increase wealth over time. It looks like that’s where you’re heading, more or less.

Thanks Ole for the stimulating post!

I wonder about the implication of this reasonable analogy. In nature or shall I say in reality (anyway I mean in everything different from a mathematical model) everything is finite, we can observe exponential growth processes only for a (maybe long but still) finite amount of time. To put it differently, explosions can’t go on forever. If any economic observable (like GDP) grows exponentially during the recent history, will this process eventually turn into a singularity that marks its end? Troy Camplin already mentioned wars. Wars above a certain devastating treshold could have such effects. On the other hand, as he mentioned too, somehow perversely, wars small enough to not impact the rest of the economy too much increase GDP, like car accidents and high expenditures for severe diseases … . On top of that GDP is a manmade construct and only a crude scalar of the multidimensional object ‘economy’ and of which many people say it resembles only little with what is important about it. That is why the Sen-Stiglitz-Fitoussi commission was put in place.

My point is the following: figures like GDP are not fundamental, the dynamic of a gamble is fundamental. Even better that there exists a scalar to make several gambles commensurable, namely the time average growth rate. This enables one to base a decision on something fundamental, maybe even something unbiased as opposed to base a decision on a figure or change of this figure that is accounts for strange things.

An often made argument against this singularity in the economic realm (econosphere) goes along the lines of “people’s wants are boundless, so is human creativity to come up with solution to please ever new wants”. The ultimate question then boils down to whether what is true for reality (biosphere or mattersphere) also has to be true for the economy (econosphere), which partly takes place in reality but also partly resides in people’s heads as the importance of expectations teaches us.

Thanks Ole for the stimulating post!

I wonder about the implication of this reasonable analogy. In nature or shall I say in reality (anyway I mean in everything different from a mathematical model) everything is finite, we can observe exponential growth processes only for a (maybe long but still) finite amount of time. To put it differently, explosions can’t go on forever. If any economic observable (like GDP) grows exponentially during the recent history, will this process eventually turn into a singularity that marks its end? Troy Camplin already mentioned wars. Wars above a certain devastating treshold could have such effects. On the other hand, as he mentioned too, somehow perversely, wars small enough to not impact the rest of the economy too much increase GDP, like car accidents and high expenditures for severe diseases … . On top of that GDP is a manmade construct and only a crude scalar of the multidimensional object ‘economy’ and of which many people say it resembles only little with what is important about it. That is why the Sen-Stiglitz-Fitoussi commission was put in place.

My point is the following: figures like GDP are not fundamental, the dynamic of a gamble is fundamental. Even better that there exists a scalar to make several gambles commensurable, namely the time average growth rate. This enables one to base a decision on something fundamental, maybe even something unbiased as opposed to base a decision on a figure or change of this figure that is accounts for strange things.

An often made argument against this singularity in the economic realm (econosphere) goes along the lines of “people’s wants are boundless, so is human creativity to come up with solution to please ever new wants”. The ultimate question then boils down to whether what is true for reality (biosphere or mattersphere) also has to be true for the economy (econosphere), which partly takes place in reality but also partly resides in people’s heads as the importance of expectations teaches us.

You open a whole box of worm cans, Mark. Let me number some of them, and then comment:

1. Can an explosion go on forever?

2. If not, how does it stop?

3. GDP increases when bad things happen.

4. GDP is a single number that misses a lot of important information.

Comments:

1. This question keeps coming up, as you rightly point out. Ken Arrow raised it as an objection after a talk I gave in Santa Fe: exponential growth cannot go on forever (my response was: I agree, but it can go on for hundreds of years). Mark Buchanan made a more nuanced version of Ken’s point — physical constraints will eventually kick in — in that case Paul Krugman objected, claiming that innovation will always make further growth possible. Mark’s summary of the debate is here: http://bit.ly/2nLaYwU

To understand whether economic growth is physical or not, you can plot the CO2 emissions of a country versus its GDP. If the relationship is monotonic, then more GDP means more fuel burned. If it’s linear, then one barrel of oil directly translates into some fixed number of dollars. The figure below shows different countries at the same point in time, so it shows that GDP is physical but doesn’t answer the question how efficiency changes over time. Does anyone have the corresponding figure over time?

2. Growth can simply fizzle out. There need not be a catastrophe. Biological organisms follow universal growth curves. When we’re small, the number of our cells grows until the energetic cost to maintain our cells balances the metabolic power supply, and we simply stop growing. There’s no law of nature that forbids maturing economies to behave similarly.

3. and 4. I would like to add that even just the mathematics cautions against using GDP and its growth to assess the health of an economy. GDP per person is precisely an ensemble average, and GDP growth — the growth rate of an ensemble average — is different from the time average growth rate, i.e. different from what an individual is likely to experience. The difference between these two growth rates, incidentally, is a good definition for the rate of change of economic inequality. Alex Adamou and I wrote this up for the Royal Statistical Society last summer: https://doi.org/10.1111/j.1740-9713.2016.00918.x

The closest thing to a nuclear explosion in economist is the ponzi scheme…

…eventually you run out of things to split, however.

The closest thing to a nuclear explosion in economist is the ponzi scheme…

…eventually you run out of things to split, however.

Pingback: Let’s pretend that people are like molecules | Real-World Economics Review Blog

Pingback: Let’s pretend that people are like molecules | Real-World Economics Review Blog

My comment concerns how to model the economy as an on-going explosion.

In my opinion, Goodwin’s business cycle could be a good starting point (Econometrica 1951, 19 (1): 1-17). It assumes generalized increasing returns. Firms invest to create and conquer ever-expanding markets, but since they compete with one another, each of them builds up a productive capacity to serve most of the market. Since it’s impossible for all of them to succeed, the crisis begins and the cycle starts again.

Unfortunately, Goodwin did not cast his model in microeconomic terms. It’s just an aggregate model.

I came across its micro-economic interpretation by reading Richardson: Information and Investment, Clarendon Press 1990.

My comment concerns how to model the economy as an on-going explosion.

In my opinion, Goodwin’s business cycle could be a good starting point (Econometrica 1951, 19 (1): 1-17). It assumes generalized increasing returns. Firms invest to create and conquer ever-expanding markets, but since they compete with one another, each of them builds up a productive capacity to serve most of the market. Since it’s impossible for all of them to succeed, the crisis begins and the cycle starts again.

Unfortunately, Goodwin did not cast his model in microeconomic terms. It’s just an aggregate model.

I came across its micro-economic interpretation by reading Richardson: Information and Investment, Clarendon Press 1990.

I would like to add a further comment.

In my opinion, capitalist economies are characterized by non-linearities stemming from generalized increasing returns to scale – either multiplicative, or exponential, or else – but they should not be likened to bombs. Explosions meet no significant resistance, whereas firms do meet resistance in penetrating markets.

My alternative analogy is rather boilling water. It makes a big difference, because boiling water meets resistance from air pressure. The flame represents the easiness with which credit is made available, but this yields no real (non-linear) growth unless firms are able to create and penetrate markets. It’s boiling water whose molecules attempt to decrease air pressure. Sometimes they succeed, but not always. In any case, they always have to make huge efforts.

Economics cannot be devoided of ideological content. The bomb analogy is marxist, for it assumes that consumers are slaves who do whatever capitalists want them to do. Equilibrium economics depicts an idealized world where consumers are souverain. The boiling water analogy has a place for both.

I would like to add a further comment.

In my opinion, capitalist economies are characterized by non-linearities stemming from generalized increasing returns to scale – either multiplicative, or exponential, or else – but they should not be likened to bombs. Explosions meet no significant resistance, whereas firms do meet resistance in penetrating markets.

My alternative analogy is rather boilling water. It makes a big difference, because boiling water meets resistance from air pressure. The flame represents the easiness with which credit is made available, but this yields no real (non-linear) growth unless firms are able to create and penetrate markets. It’s boiling water whose molecules attempt to decrease air pressure. Sometimes they succeed, but not always. In any case, they always have to make huge efforts.

Economics cannot be devoided of ideological content. The bomb analogy is marxist, for it assumes that consumers are slaves who do whatever capitalists want them to do. Equilibrium economics depicts an idealized world where consumers are souverain. The boiling water analogy has a place for both.

Pingback: Kanssalaisyhteiskunta 2. osa: Tuottaja, kaupunkilainen, työläinen – Volanen vasemmalta

Pingback: Kanssalaisyhteiskunta 2. osa: Tuottaja, kaupunkilainen, työläinen – Volanen vasemmalta

Pingback: Köyhyys, tasa-arvo ja ympäristö – Volanen vasemmalta

Pingback: Köyhyys, tasa-arvo ja ympäristö – Volanen vasemmalta

Pingback: Sundry: Purpose, wikiHow, negotiations, the illusion of transparency, cannabis – Ulysse Sabbagh