The most interesting scientific projects are those that surprise, when the mathematics, or the code, tells us something we didn’t expect. In our study of US wealth dynamics that’s what happened. We wrote it up in a paper, but that’s only the end product not the curious route by which we got there. Hence this post.

The equation of life

We started thinking about wealth dynamics some time in 2010 or 2011. We had been studying ensembles of growth processes, and that naturally led to thinking about ensembles of people and their growing wealths. Here’s what we did (“we” being Yonatan Berman, Alex Adamou, and I): we started with a ridiculously simple model for personal wealth, namely geometric Brownian motion (GBM).

(1) dx=x(\mu dt + \sigma dW)

I like to call this the equation of life. Why? Because life can be (and has been) defined as the thing that self-reproduces, and that’s what the equation describes. A quantity x that produces more of itself in a noisy way. It describes what happens to the biomass of an embryo in its early stages of development, or to the population of some species growing in a rich environment.

Once we’ve got self-reproduction in an environment with some fluctuations, evolution gets going, and beautiful structures like the ones we see around us follow sooner or later.

Equation (1) doesn’t just model biomass or populations but is also quite good at describing stock price dynamics. So we thought that it may be good at describing personal wealth too. After all, in one way or another both the stock market and our monetary fortunes reflect something that is happening in the economy. Let’s actually name the thing: we’re talking about capitalism. The genius of capitalism is precisely its multiplicative nature. Unused resources — capital — can be deployed to produce more of themselves. In this way a capitalist economy resembles the basic dynamic of evolution.

Our model does resemble wealth in a capitalist structure, but we were aware of its simplifying assumptions. It pretends that any changes in wealth are proportional to current wealth, whereas I could be poor and nonetheless boost my wealth through earned income. We treat everyone the same and pretend that differences in skill or earnings potential are random and not persistent etc. Nonetheless, we were curious about what would happen in a world where people’s wealth simply followed GBM.

Re-allocation: stability, Pareto tail, middle class

The first observation is this: under GBM the distribution of wealth never stabilizes, not even relative wealth stabilizes (that’s personal wealth divided by total population wealth). If we wait for long enough, essentially one person ends up with all the wealth. That struck us as unrealistic: we don’t live under feudalism. But we used to live under feudalism, so the real dynamic must be less extreme than GBM. That makes some sense — after all, the government collects taxes, and there are institutions that fund all sorts of social programs. We decided to make the model a little more realistic and included re-allocation of wealth. Surely the poor are helped by the rich in some way. So we changed the equation to

(2) dx=x([\mu-\tau] dt + \sigma dW) + \tau \langle x \rangle_N dt.

The new terms say this: every year everyone in the economy contributes a proportion \tau of his wealth to a central pot, and then the pot is split evenly across the population ( \langle x \rangle_N is per-capita wealth). Again, this is very simplistic — \tau represents a lot of different effects: collective investment in infrastructure, education, social programs, taxation, rents paid, private profits made… The equation can be re-written, which is very neat.

(3) dx=x(\mu dt + \sigma dW) - \tau (x- \langle x \rangle_N) dt.

This shows that it’s just like GBM (the first term) plus a mean-reversion process that attracts wealth to the population average. If I’m richer than the average, I’m likely to become a little poorer (relative to the average — my wealth can still grow); if I’m poorer I’m likely to become a little richer. The strength of the reversion is \tau, which can be thought of as a social cohesion parameter.

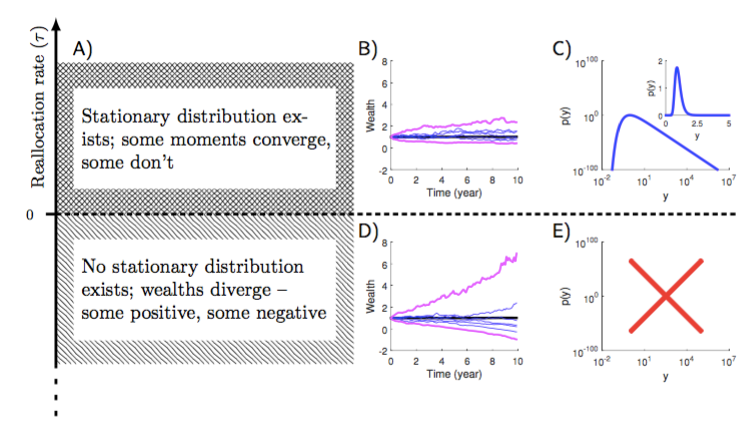

This equation is great! Whereas GBM leads to a diverging (unstable) log-normal distribution of relative wealth, equation (3) leads to a stationary inverse-gamma distribution. I mean if you let the equation run for a while, the number of people with a given wealth will follow an inverse gamma distribution. That distribution has a power-law tail, similar to what has been observed many times since Pareto‘s first studies. So it’s already pretty good, on a coarse-grained level.

What else did we know? Under GBM, wealth cannot become negative. Since the poor are always better off under equation (2), this is also true here.

Enter the computer

Thanks to tremendous efforts by many authors, including Tony Atkinson, Thomas Piketty, Emmanuel Saez, Gabriel Zucman, Wojciech Kopcuk, Jesse Bricker, Alice Henriques, Jacob Krimmel, and John Sabelhaus, we have a fairly good idea of the US wealth distribution over the past 100 years. So we took those observed distributions, created 100,000,000 individuals on a computer, fixed \mu directly from the wealth data and set \sigma roughly to the values observed in the stock market, and let the computer tune \tau each year so as to reproduce the real distributions.

Just for fun, we then looked at the individual wealths that had been produced by this procedure, and we noticed something strange. Many of them were negative. So back to the code, what did we do wrong? An error in the discretization scheme? Some other bug? No, the effect was real.

Negative re-allocation

Here’s what happened: in order to reproduce the data, towards the end of the analyzed period the algorithm had to make \tau negative, see figure 2 below. But what happens under those conditions to equation (3)?

Well, it describes negative re-allocation. Everyone pays the same dollar amount into a central pot, and then everyone receives from the pot an amount in proportion to how much he already has. That means if I have nothing, then I receive nothing but I still have to pay. That can make my wealth negative.

Look at equation (3) again, imagining \tau to be negative. The second term now describes mean repulsion. Whereas before wealth was attracted to the population mean, which generates a middle class, now wealth is repelled from it. If I’m a bit richer than the average, I’ll be boosted up even further; if I’m a little poorer, I’ll be pushed down even further. Run this equation for a little while and a large class of negative-wealth individuals arises.

At is turns out, something like that exists in reality. The cumulative wealth of the poorer half of the American population is roughly zero, meaning there must be a large class of negative-wealth individuals.

Falling interest rates

This is a blog post, so let me be speculative and push the story a little further than in the paper. How do those who have less than nothing keep giving to the rich? Simple: they go deeper into debt, deeper into negative wealth. But how can that be sustained over a long time? Debts don’t need to be paid off, but they do need to be serviced. To service growing debt with stagnant income (the situation in the US roughly since 1980), we need to lower interest rates.

Interest rates have been falling since about 1980, see Figure 4, precisely the time when the re-allocation rate became negative (c.f. Figure 1). What if there’s a causal link?

Now it gets interesting: interest rates have hit zero. What do we do? How can the poor keep paying the rich? Sure, let’s have some quantitative easing, but can that go on forever? Or will it break at some point? Is redistribution from poor to rich a threat to our monetary system? Is it a threat to our democracy? Where does the system go from here?

Let’s be clear about what we’ve done. We built a simple model and fitted its one main parameter. This wraps everything that’s actually happening into this one parameter. There are loose ends — the model may be fooling us, but we’re certainly not in a regime where we can comfortably rely on stabilization. We don’t claim that the world really works like equation 2, but that’s not the point of the exercise. Instead we say “pretend that equation 2 describes the dynamics of wealth; what parameter values would then best resemble what really happens?” The model is no more than a model and as such brushes over many details. For example, we don’t explicitly treat inheritance or income tax or some specific welfare program. Rather, this is all treated implicitly: our \tau summarizes everything that affects the wealth distribution beyond the null model of GBM. It reflects the overall trend in the complete economic system.

Ergodicity

That the model produced behavior beyond our (initial) imagination is encouraging. It means we didn’t accidentally constrain our study to confirm our beliefs. We wanted to know by how much we need to slow down the increase in wealth inequality implied by GBM to get to a realistic model. The model said: no, you’re asking the wrong question. GBM actually understates the increase in wealth inequality, and you need to correct the other way. Under GBM relative wealth is non-ergodic. The ergodic hypothesis as it is made in studies of wealth inequality thus excludes GBM as too extreme. Now it turns out that real wealth dynamics are better described by correcting GBM to make it even more strongly non-ergodic. None of us had expected that.

We should have written down our guesses for \tau before we started the study. We didn’t do this, but we certainly thought we would find a positive value. In a private correspondence, from the time before we looked at the data, Jean-Philippe Bouchaud set \tau =5\% p.a. in an example calculation, and we all felt that was the right order of magnitude. It could be 2% but obviously not as small as 0% (which would be GBM, equation 1).

Time scales

The connection to interest rates is speculative, but here’s one rock solid message about time scales that may hint at how we got here. A change in the effective re-allocation rate, \tau, takes decades to feed through. These processes operate on time scales of generations, not election cycles. That means it’s easy to oversteer because the consequences of policy changes only become visible after 30 or 50 years, long after whoever made the policy changes has left office, and at a time when the reasons for making the changes may no longer be valid. We certainly mustn’t assume rapid equilibration. However, rapid equilibration — the ergodic hypothesis — is a standard assumption in studies of wealth distributions.

The basic dynamic of a multiplicative-wealth economy — capitalism — seems underappreciated to me. If we “do nothing” ( \tau =0), inequality increases indefinitely. If we re-distribute fast enough ( \tau>0), inequality will stabilize at some level. If we actively destabilize ( \tau<0) as we seem to have done in recent decades, the middle class vanishes and we create a division between rich and poor — a poor person behaving reasonably is as unlikely to become middle class as a rich person behaving reasonably.

——

p.s. we can make the model arbitrarily complex. One aspect we later singled out is the effect of earnings, by including observed earnings in equation (2). Usually earnings have a stabilizing effect (meaning the process that describes only wealth must be less stable when earnings are treated explicitly). In the last 10 years or so, that stabilizing effect has been absent because of earnings inequality. Consequently, the values we find for \tau with this version of the model are smaller (more negative) up until about 2000 and then unchanged, see figure 5 below.

Curious about Ergodicity Economics?

Join our mailing list.

Seriously curious?

Get a copy of the textbook:

Enjoyed your post again. You said GBM “ridiculously simple model”. But it captures almost all essential dynamics. Simplicity is good.

Enjoyed your post again. You said GBM “ridiculously simple model”. But it captures almost all essential dynamics. Simplicity is good.

Lost me when you wrote: “We treat everyone the same and pretend that differences in skill or earnings potential are random and not persistent etc.”

Thank you for your comment, Scott. It’s not easy to say in words what an equation does, and you’re right that this sentence is not strictly correct. The following is correct: all individuals are modelled with the same parameter values and

and  . There are no differences at this level.

. There are no differences at this level.

However, it’s sloppy to turn this into English by saying that “we treat everyone the same.” Let me try to make a few correct statements that also explain a little bit why this model is so strangely powerful.

1: individuals are fully characterised by their wealth — that’s the only idiosyncratic property we keep track of. Although wealth generally changes with time in the model, it is also persistent: if an individual is rich this year it will not suddenly be poor next year, maybe a bit less rich, but wealths don’t jump around.

2: that means the distribution of individual wealth changes also doesn’t jump around, but it also changes gradually, so there’s persistence in that too, which you could interpret as persistence in earnings potential or skill. Mathematically speaking, there are strong temporal correlations in the changes of wealth of any one individual. This is a feature of GBM that the model maintains (and that’s different from just Brownian motion).

3: wealth in the model does not just set the scale of future wealth changes. Rather, because there’s that re-allocation mechanism — being rich can mean paying systematically more or paying systematically less into the common pot. Individuals are therefore treated differently in this respect.

4: everyone experiences a different realization of the noise, so we don’t treat everyone the same in that sense either — randomly some win, some lose.

5: at the beginning of the numerical analysis we set wealths so as to resemble the wealth distribution of 1918, meaning from the beginning there are differences in wealth and not everyone is the same, with the consequences described above.

The sentence you quote had two aims: it highlights the simplicity of the model (a good thing), and it warns against using the model outside its domain of applicability. It’s well suited to the purpose of our study, but that doesn’t mean it’s well suited to all studies of wealth distribution. For example, it doesn’t distinguish between male and female, so I can’t study gender differences with it.

Why people have more or less is a very important question, but we’re setting that aside. If you’re rich, you’ll probably stay rich for a while. That’s all the model knows. We just ask where the net flows are going. To assess _what_ happens, in this case, we don’t need to know precisely _why_ it happens, and therefore we can make simplifying assumptions that ignore the “why” but don’t affect the “what.”

By throwing out details, we make the model simple, and we can begin to understand systemic stability, from a bird’s eye perspective. Whether it’s because of talent, hard work, ability, luck or anything else — if flows go systematically from poor to rich, then the middle class disappears. Many will find themselves in debt they cannot repay, and some will find themselves in wealth they can’t consume.

I should also say that this is not a value judgement, it just lays out the naked mechanics. We may want to concentrate wealth and power in the hands of a small elite, corresponding to (that's seems to be what we're doing at the moment). Royalists have argued that that’s a good thing, and feudal societies are organized that way. At the other extreme communists would argue that

(that's seems to be what we're doing at the moment). Royalists have argued that that’s a good thing, and feudal societies are organized that way. At the other extreme communists would argue that  is a good thing — like in feudalism, private property doesn’t strictly exist in communism. Capitalist democrats tend to be somewhere in the middle, they might want

is a good thing — like in feudalism, private property doesn’t strictly exist in communism. Capitalist democrats tend to be somewhere in the middle, they might want  , something small but positive. What value of

, something small but positive. What value of  a society aims for is a political choice. In our work we’re just helping to measure it so that people can have an informed debate about the the choices we want to make as a society.

a society aims for is a political choice. In our work we’re just helping to measure it so that people can have an informed debate about the the choices we want to make as a society.

This point of view becomes so true in this days. Almost prophetic! Thanks for the blog!

This has some similarities in form and conclusion to an IBM described in:

Fargione JE, Lehman C, Polasky S (2011) Entrepreneurs, Chance, and the Deterministic Concentration of Wealth. PLoS ONE 6(7): e20728. https://doi.org/10.1371/journal.pone.0020728

Thank you, Richard. I had a quick look at the paper. They study GBM, meaning re-allocation rate . Even GBM itself is a fabulously powerful model, but one thing it cannot explain is falling or stable inequality. There have been periods in history when wealth inequality dropped, and that cannot be reproduced with GBM. With RGBM (re-allocating geometric Brownian motion), such periods can be represented with a positive reallocation rate,

. Even GBM itself is a fabulously powerful model, but one thing it cannot explain is falling or stable inequality. There have been periods in history when wealth inequality dropped, and that cannot be reproduced with GBM. With RGBM (re-allocating geometric Brownian motion), such periods can be represented with a positive reallocation rate,  .

.

Under GBM, as the authors show, a vanishing proportion of the population ends up with all the wealth. That means the system does not properly equilibrate and does not satisfy the ergodicity conditions that for some reason many researchers require of their models. It’s a strange belief in the field: the model has to be ergodic, otherwise it’s not economic science. But that excludes GBM from the set of models that are allowed. Because of this unnecessary restriction not even these very simple models (GBM or RGBM) have been properly explored in this context.

This has some similarities in form and conclusion to an IBM described in:

Fargione JE, Lehman C, Polasky S (2011) Entrepreneurs, Chance, and the Deterministic Concentration of Wealth. PLoS ONE 6(7): e20728. https://doi.org/10.1371/journal.pone.0020728

Thank you, Richard. I had a quick look at the paper. They study GBM, meaning re-allocation rate . Even GBM itself is a fabulously powerful model, but one thing it cannot explain is falling or stable inequality. There have been periods in history when wealth inequality dropped, and that cannot be reproduced with GBM. With RGBM (re-allocating geometric Brownian motion), such periods can be represented with a positive reallocation rate,

. Even GBM itself is a fabulously powerful model, but one thing it cannot explain is falling or stable inequality. There have been periods in history when wealth inequality dropped, and that cannot be reproduced with GBM. With RGBM (re-allocating geometric Brownian motion), such periods can be represented with a positive reallocation rate,  .

.

Under GBM, as the authors show, a vanishing proportion of the population ends up with all the wealth. That means the system does not properly equilibrate and does not satisfy the ergodicity conditions that for some reason many researchers require of their models. It’s a strange belief in the field: the model has to be ergodic, otherwise it’s not economic science. But that excludes GBM from the set of models that are allowed. Because of this unnecessary restriction not even these very simple models (GBM or RGBM) have been properly explored in this context.

Thanks for the fascinating post. I especially like your “equation of life” interpretation. I’ll remember that one.

Something that stands out when I look at your plots is that the noise of unaveraged tau seems large relative to its moving average. Do you agree? I wonder if it can be reduced… perhaps with more trials? Or with a change to the model? Or is it possible that tau is one of your weak ergodicity breaking variables?

On the other hand, perhaps the unaveraged (black) tau line is even more informative than the average, and is telling us something about the contemporaneous state of the economy. To my naked eye, it appears that tau is more positive in the “garden variety” recessions of the early 80’s, early 90’s, and early 2000’s. (And in the wild crash of 1929-30.) But not during the credit crisis of 2008. Some factors to investigate might be unemployment insurance, declines in stock market wealth (which disproportionately affect the wealthier among us), and personal bankruptcies (which help the least wealthy get a fresh start). (But the dynamics of these factors were very different in 1930 compared to 2000.)

To explain the recent negativity of (averaged) tau, you have mentioned interest rates as a possible contributor. On a related note, perhaps home-ownership is a contributor too… The less wealthy typically don’t own homes. In many markets, homes have greatly increased in value, hand-in-hand with the decline in interest rates, which enables the the wealthier to afford increasingly larger mortgages. It might be interesting to fit the model to different metro areas, to compare those with more home price appreciation to those with less.

Thanks again for the great work. Your ideas are among the most exciting ones to hit financial economics in a long time.

Hi Patrick, thanks for your comment. I am one of the paper’s co-authors. Regarding the noise in , we cannot have more trials, because we only have one – the reality. That being said, we show in the paper that the averaging process does not introduce artificial biases and essentially captures the information in the non-averaged

, we cannot have more trials, because we only have one – the reality. That being said, we show in the paper that the averaging process does not introduce artificial biases and essentially captures the information in the non-averaged  (see figure 4 in http://papers.ssrn.com/abstract=2794830).

(see figure 4 in http://papers.ssrn.com/abstract=2794830).

Thanks for the fascinating post. I especially like your “equation of life” interpretation. I’ll remember that one.

Something that stands out when I look at your plots is that the noise of unaveraged tau seems large relative to its moving average. Do you agree? I wonder if it can be reduced… perhaps with more trials? Or with a change to the model? Or is it possible that tau is one of your weak ergodicity breaking variables?

On the other hand, perhaps the unaveraged (black) tau line is even more informative than the average, and is telling us something about the contemporaneous state of the economy. To my naked eye, it appears that tau is more positive in the “garden variety” recessions of the early 80’s, early 90’s, and early 2000’s. (And in the wild crash of 1929-30.) But not during the credit crisis of 2008. Some factors to investigate might be unemployment insurance, declines in stock market wealth (which disproportionately affect the wealthier among us), and personal bankruptcies (which help the least wealthy get a fresh start). (But the dynamics of these factors were very different in 1930 compared to 2000.)

To explain the recent negativity of (averaged) tau, you have mentioned interest rates as a possible contributor. On a related note, perhaps home-ownership is a contributor too… The less wealthy typically don’t own homes. In many markets, homes have greatly increased in value, hand-in-hand with the decline in interest rates, which enables the the wealthier to afford increasingly larger mortgages. It might be interesting to fit the model to different metro areas, to compare those with more home price appreciation to those with less.

Thanks again for the great work. Your ideas are among the most exciting ones to hit financial economics in a long time.

Hi Patrick, thanks for your comment. I am one of the paper’s co-authors. Regarding the noise in , we cannot have more trials, because we only have one – the reality. That being said, we show in the paper that the averaging process does not introduce artificial biases and essentially captures the information in the non-averaged

, we cannot have more trials, because we only have one – the reality. That being said, we show in the paper that the averaging process does not introduce artificial biases and essentially captures the information in the non-averaged  (see figure 4 in http://papers.ssrn.com/abstract=2794830).

(see figure 4 in http://papers.ssrn.com/abstract=2794830).

Pingback: New top story on Hacker News: Wealth: redistribution and interest rates – The Internet Yard

Pingback: New top story on Hacker News: Wealth: redistribution and interest rates – The Internet Yard

Pingback: Wealth: redistribution and interest rates | ExtendTree

Pingback: Wealth: redistribution and interest rates | ExtendTree

Pingback: Wealth: redistribution and interest rates via /r/economy | Chet Wang

Pingback: Wealth: redistribution and interest rates via /r/economy | Chet Wang

Economists seem to be totally oblivious to this sad predicament even 10 years after the financial crisis. Now, we can no longer lower rates any further and bringing them could cause the whole debt pile to collapse. The US economy is almost in a type of purgatory.

Economists seem to be totally oblivious to this sad predicament even 10 years after the financial crisis. Now, we can no longer lower rates any further and bringing them could cause the whole debt pile to collapse. The US economy is almost in a type of purgatory.

How do you account for wars, severe crises etc…? It seemed to me that GBM is not the right choice for describing how wealth fluctuates through time. For instance Piketty observes that wars triggered decreases in inequality. History seems to be shaped by a few points but with large magnitude effects.

Thanks for your comment, Eric. Just to make sure we’re talking about the same thing: we don’t use GBM, equation 1, for describing how wealth fluctuates through time. We use equation 2, namely what we call “RGBM” (re-allocating geometric Brownian motion). One reason for adding the extra terms is that GBM alone never generates decreases in inequality, but these do occur in history, as you say.

What we did does not contradict Thomas Piketty’s observations. Quite the opposite — some of the data we analyse were collected and prepared by Piketty and Gabriel Zucman. Have a look at Figure 2, above. In the 1930s and 1940s you see large effective re-allocation rates, corresponding to decreases in inequality. Yonatan Berman, the lead author of the study is currently in Paris working with Piketty and his group, and we’re learning how better to connect the different approaches of interpreting the data.

Thanks Ole, Great to know that you join forces with Thomas. My question was more related to the Wiener process you use to model the stochastic part. Is it not too mild? I do like your reallocation mechanism. It makes sense. However one question still haunts me. I do understand that inequality can only be judged dynamically. Indeed, (in your words) ” If rescaled wealth were an ergodic process, then individuals would, over long enough time, experience all parts of its distribution.” Which would mean a dynamically equal society. Is it fair to conclude that your reallocation variable “thau” reflects different periods of balance of power in history. When thau is negative the rent seekers have won, social mobility is “frozen”. But for how long does Thau have to remain negative to conclude that society is truly unequal? Do you fear that in a digital economy with very strong winner take all effects, the rent seekers may win for good? They may indeed have more leverage to push and maintain thau in negative territories. In other words what’s the political economy behind (or underlying) thau? Does negative thau correspond to the periods where Piketty claims (r > g, his famous inequality)?

How do you account for wars, severe crises etc…? It seemed to me that GBM is not the right choice for describing how wealth fluctuates through time. For instance Piketty observes that wars triggered decreases in inequality. History seems to be shaped by a few points but with large magnitude effects.

Thanks for your comment, Eric. Just to make sure we’re talking about the same thing: we don’t use GBM, equation 1, for describing how wealth fluctuates through time. We use equation 2, namely what we call “RGBM” (re-allocating geometric Brownian motion). One reason for adding the extra terms is that GBM alone never generates decreases in inequality, but these do occur in history, as you say.

What we did does not contradict Thomas Piketty’s observations. Quite the opposite — some of the data we analyse were collected and prepared by Piketty and Gabriel Zucman. Have a look at Figure 2, above. In the 1930s and 1940s you see large effective re-allocation rates, corresponding to decreases in inequality. Yonatan Berman, the lead author of the study is currently in Paris working with Piketty and his group, and we’re learning how better to connect the different approaches of interpreting the data.

Thanks Ole, Great to know that you join forces with Thomas. My question was more related to the Wiener process you use to model the stochastic part. Is it not too mild? I do like your reallocation mechanism. It makes sense. However one question still haunts me. I do understand that inequality can only be judged dynamically. Indeed, (in your words) ” If rescaled wealth were an ergodic process, then individuals would, over long enough time, experience all parts of its distribution.” Which would mean a dynamically equal society. Is it fair to conclude that your reallocation variable “thau” reflects different periods of balance of power in history. When thau is negative the rent seekers have won, social mobility is “frozen”. But for how long does Thau have to remain negative to conclude that society is truly unequal? Do you fear that in a digital economy with very strong winner take all effects, the rent seekers may win for good? They may indeed have more leverage to push and maintain thau in negative territories. In other words what’s the political economy behind (or underlying) thau? Does negative thau correspond to the periods where Piketty claims (r > g, his famous inequality)?

Hi Ole, any thought on my previous rumination ;-)?

Thank you for elaborating. Let me split your comment into two topics, namely 1) Gaussian noise and 2) the meaning of tau.

Gaussian noise:

First, let’s keep the main message in mind, which may not even be empirical but methodological. Studies of wealth distributions assume, often explicitly, that real (relative) wealth is well modelled with an ergodic stochastic process on humanly relevant time scales. That means we just have to wait — irrespective of economic, political, social conditions — and the wealth distribution will settle into its stationary form. Our point is that that may be a misrepresentation of reality. We can be in a regime where things simply fly apart, and the longer we wait the further they fly apart. In the relevant models, no ergodic distribution exists. Anyone who thinks about policy needs to be aware of this. But the current dominant (exclusive) belief is that an ergodic model is always good on humanly relevant time scales. That’s clearly not true.

Specifically about the Gaussian noise, of course you’re right that more detail could be added to the noise. But we choose not to do that. We use Gaussian noise for the usual reason, i.e. because of its roles as an attractor of distributions under convolution (the Gaussian central limit theorem). We think that’s at least a starting point because it’s not unreasonable to think of someone’s wealth as the result of many successive investments over time (“investments” in health, education, stock markets etc). In some limit these would convolve to something like Gaussian noise.

Where we put the Gaussian assumption is important. The model in Equation 2 (RGBM) is impressively powerful: we do put Gaussian noise into the relative changes of people’s wealth (before re-allocation). But the resulting wealth distribution is very much not Gaussian, and close to what’s observed. If tau is positive (details in the paper), equation 2 generates relative wealth distributed according to an inverse gamma distribution. The model happens to be analytically solvable (with Gaussian noise). An inverse gamma distribution has a power-law tail, which is precisely what Pareto observed in wealth distributions early in the 20th century. So this very simple model fits surprisingly well with the known big picture.

Interpretation of tau:

I think you have a good understanding of the flavour of what tau means, but I don’t want to think about that too much. The precise mechanisms that set tau are so numerous that it’s easy to get lost in the details — is this a change in taxation, in technology, demography, credit availability, interest rates, tuition fees, corporate profitability, asset valuations, public versus private ownership… it’s a long list of possible causes. But roughly: yes, where technological development leads to large concentrations of wealth, tau will become negative. The hope, of course, is that we will all enjoy the fruits of technological progress — like online university education at a fraction of the cost of traditional degrees. But that’s not a given. We’re raising a red flag here: careful, this kind of thing can have unintended consequences that are currently not considered in the academic literature and apparently not well understood by policy makers either.

Thanks Ole. This confirms my own intuition. I agree on your first point predicated on less is (finally) more;-) My background is economics, insurance and finance (https://scholar.google.be/citations?user=OydygRoAAAAJ&hl=fr) As you know there has been a lot of academic debate on brownian motion, mixed jump-diffusion processes, mild vs. wild etc… In my own research I used both brownian and jump. Hence my question. On tau, I do want to think about it 😉 as this is what gives your results real strength. I think you should too 😉 You’re on to something that could end up big. Your results show in a very elegant manner that the devil lies in the details, that the path to ergodicity is incredibly difficult (something Douglass C North discussed in https://scholarship.law.duke.edu/cgi/viewcontent.cgi?referer=https://duckduckgo.com/&httpsredir=1&article=1165&context=delpf) , that the inequality debate is awfully complex with many higher order effects hidden in tau. This is where science meets political economy and that’s not that frequent. Nassim would tell you that skin in the game is the solution, that it will bring tau back in positive territory, that it will restore ergodicity. I am not sure that is that simple even if on paper it looks promising.

Thanks Ole. This confirms my own intuition. I agree on your first point predicated on less is (finally) more;-) My background is economics, insurance and finance (https://scholar.google.be/citations?user=OydygRoAAAAJ&hl=fr) As you know there has been a lot of academic debate on brownian motion, mixed jump-diffusion processes, mild vs. wild etc… In my own research I used both brownian and jump. Hence my question. On tau, I do want to think about it 😉 as this is what gives your results real strength. I think you should too 😉 You’re on to something that could end up big. Your results show in a very elegant manner that the devil lies in the details, that the path to ergodicity is incredibly difficult (something Douglass C North discussed in https://scholarship.law.duke.edu/cgi/viewcontent.cgi?referer=https://duckduckgo.com/&httpsredir=1&article=1165&context=delpf) , that the inequality debate is awfully complex with many higher order effects hidden in tau. This is where science meets political economy and that’s not that frequent. Nassim would tell you that skin in the game is the solution, that it will bring tau back in positive territory, that it will restore ergodicity. I am not sure that is that simple even if on paper it looks promising.

Hi Ole, any thought on my previous rumination ;-)?

Thank you for elaborating. Let me split your comment into two topics, namely 1) Gaussian noise and 2) the meaning of tau.

Gaussian noise:

First, let’s keep the main message in mind, which may not even be empirical but methodological. Studies of wealth distributions assume, often explicitly, that real (relative) wealth is well modelled with an ergodic stochastic process on humanly relevant time scales. That means we just have to wait — irrespective of economic, political, social conditions — and the wealth distribution will settle into its stationary form. Our point is that that may be a misrepresentation of reality. We can be in a regime where things simply fly apart, and the longer we wait the further they fly apart. In the relevant models, no ergodic distribution exists. Anyone who thinks about policy needs to be aware of this. But the current dominant (exclusive) belief is that an ergodic model is always good on humanly relevant time scales. That’s clearly not true.

Specifically about the Gaussian noise, of course you’re right that more detail could be added to the noise. But we choose not to do that. We use Gaussian noise for the usual reason, i.e. because of its roles as an attractor of distributions under convolution (the Gaussian central limit theorem). We think that’s at least a starting point because it’s not unreasonable to think of someone’s wealth as the result of many successive investments over time (“investments” in health, education, stock markets etc). In some limit these would convolve to something like Gaussian noise.

Where we put the Gaussian assumption is important. The model in Equation 2 (RGBM) is impressively powerful: we do put Gaussian noise into the relative changes of people’s wealth (before re-allocation). But the resulting wealth distribution is very much not Gaussian, and close to what’s observed. If tau is positive (details in the paper), equation 2 generates relative wealth distributed according to an inverse gamma distribution. The model happens to be analytically solvable (with Gaussian noise). An inverse gamma distribution has a power-law tail, which is precisely what Pareto observed in wealth distributions early in the 20th century. So this very simple model fits surprisingly well with the known big picture.

Interpretation of tau:

I think you have a good understanding of the flavour of what tau means, but I don’t want to think about that too much. The precise mechanisms that set tau are so numerous that it’s easy to get lost in the details — is this a change in taxation, in technology, demography, credit availability, interest rates, tuition fees, corporate profitability, asset valuations, public versus private ownership… it’s a long list of possible causes. But roughly: yes, where technological development leads to large concentrations of wealth, tau will become negative. The hope, of course, is that we will all enjoy the fruits of technological progress — like online university education at a fraction of the cost of traditional degrees. But that’s not a given. We’re raising a red flag here: careful, this kind of thing can have unintended consequences that are currently not considered in the academic literature and apparently not well understood by policy makers either.

Thanks Ole. This confirms my own intuition. I agree on your first point predicated on less is (finally) more;-) My background is economics, insurance and finance (https://scholar.google.be/citations?user=OydygRoAAAAJ&hl=fr) As you know there has been a lot of academic debate on brownian motion, mixed jump-diffusion processes, mild vs. wild etc… In my own research I used both brownian and jump. Hence my question. On tau, I do want to think about it 😉 as this is what gives your results real strength. I think you should too 😉 You’re on to something that could end up big. Your results show in a very elegant manner that the devil lies in the details, that the path to ergodicity is incredibly difficult (something Douglass C North discussed in https://scholarship.law.duke.edu/cgi/viewcontent.cgi?referer=https://duckduckgo.com/&httpsredir=1&article=1165&context=delpf) , that the inequality debate is awfully complex with many higher order effects hidden in tau. This is where science meets political economy and that’s not that frequent. Nassim would tell you that skin in the game is the solution, that it will bring tau back in positive territory, that it will restore ergodicity. I am not sure that is that simple even if on paper it looks promising.

Thanks Ole. This confirms my own intuition. I agree on your first point predicated on less is (finally) more;-) My background is economics, insurance and finance (https://scholar.google.be/citations?user=OydygRoAAAAJ&hl=fr) As you know there has been a lot of academic debate on brownian motion, mixed jump-diffusion processes, mild vs. wild etc… In my own research I used both brownian and jump. Hence my question. On tau, I do want to think about it 😉 as this is what gives your results real strength. I think you should too 😉 You’re on to something that could end up big. Your results show in a very elegant manner that the devil lies in the details, that the path to ergodicity is incredibly difficult (something Douglass C North discussed in https://scholarship.law.duke.edu/cgi/viewcontent.cgi?referer=https://duckduckgo.com/&httpsredir=1&article=1165&context=delpf) , that the inequality debate is awfully complex with many higher order effects hidden in tau. This is where science meets political economy and that’s not that frequent. Nassim would tell you that skin in the game is the solution, that it will bring tau back in positive territory, that it will restore ergodicity. I am not sure that is that simple even if on paper it looks promising.

thanks

thanks

This is fascinating – it seems that the model does describe the US economy. Have you tried to model more “social-democratic” economies to see if it holds up? And, as a geek, I’d love to see the code – I couldn’t find a link in the paper.

This is fascinating – it seems that the model does describe the US economy. Have you tried to model more “social-democratic” economies to see if it holds up? And, as a geek, I’d love to see the code – I couldn’t find a link in the paper.

It’s not so much about whether the model holds up. We can fit the model to different data (from different countries or time periods), and the best-fit parameters will be different. The key advantage of this model is that — unlike other models — it allows us to see conditions that are not long-term stable. Other models put in long-term stability as an assumption (the ergodic hypothesis); we get a measure out that tells us whether the system is stable or not, and what the associated time scales of convergence or divergence are. Code is not publicly available yet.

It’s not so much about whether the model holds up. We can fit the model to different data (from different countries or time periods), and the best-fit parameters will be different. The key advantage of this model is that — unlike other models — it allows us to see conditions that are not long-term stable. Other models put in long-term stability as an assumption (the ergodic hypothesis); we get a measure out that tells us whether the system is stable or not, and what the associated time scales of convergence or divergence are. Code is not publicly available yet.

Thanks for a very insightful model and interesting post. I’d like to ask to you a couple of questions: (1) If timescale for wealth redistribution policies can only produce effects past 30-50 years, it is logical to expect that survival mechanisms will attract a faster violent/turbulent response for di facto wealth redistribution before it is too late for that generation. Is there a way to model the risk of falling into turbulent economic times (wars, dictatorships, massive ruins, economic depressions) once wealth inequality raises critical levels? As it happens with physics of fluids, could a kind of “Reynolds numbers” for inequality be a guide for determining the right policy for a particular situation? (2) If redistributions policies are not effective, avoiding the redistribution problem may lead to a solution. If there is a mechanism by which each individual could certificate her/his own creation of wealth – I mean, wealth would be already distributed by its creation (no debt needed), would the RGBM model of capital concentration derive again to an inequality situation similar to what is happening in the USA nowadays?

I should emphasize that we’re not explicitly modeling taxation. We just ask, with respect to the null model of geometric Brownian motion: what is the current overall re-allocating (or re-distributive) effect of the entire economic system. At its most re-allocating times that would have stabilized the distribution, or mixed it, within 30-50 years. At the moment it doesn’t do that, so the time scale is infinite (or doesn’t exist). Your question (1) is troubling, of course. I don’t know the answer but we have to take it seriously. There are many contributing factors (monetary policy and technological change being two of them). Changes to those could change the picture. It is also possible that we transition peacefully into feudalism (not saying that’s a good thing). I’m not sure what you mean by (2); at the moment a lot of wealth is created by algorithms, and quantifying what activity creates wealth is impossible — did the uber driver taking the silicon valley entrepreneur to a crucial meeting create a billion dollars?

Thanks for the clarifications! I’d like to reformulate my second question as follows: (2) Having a direct mechanism of re-distribution of wealth like a UBI system, would the RGBM model end up stabilized? What percentage of wealth should the UBI system take to get the model stabilized in the USA?

The RGBM model stabilizes, in practice, for positive re-allocation rates.

A universal basic income, to first order, would increase the re-allocation rate and may make it positive, so the wealth distribution would become stabilizing. The issue is that this is “to first order” and people argue over higher-order effects, which may be significant.

It is interesting that reallocation hovers around zero — that just means that GBM without corrections is a pretty good model. Perhaps it also means that whatever intervention you come up with, the system will reconfigure itself into something close to GBM.

But reallocating 1% of wealth per year would make an immediate big difference.

Here’s an interesting number: total US federal revenue is about $3.7tn. Total personal wealth in the US is about $100tn. At the moment, you could set all federal tax to zero and replace it with a flat wealth tax of 3.7% per year.

That’s an impressive number! It is hard to understand why with such a potential low tax rate to eliminate the public deficit, the public debt has systematically raised. This discrepancy might suggest a shadow expenditure that gets the benefit of being financed by debt. Or as you have suggested, the reduction of interest rates might have obligated the permanent rescue of the financial system by governments. Wouldn’t that be a systematic pressure from the financial system on governments? Well, enough speculation from my part! Thank you very much for sharing quite interesting numbers and for your very concise answers. I appreciate the time given to my questions on this fascinating topic. I will read the paper carefully and try to apply the model to other countries. I am particularly interested in Switzerland and Norway; both with a similar level of wealth but the first relies more on the free market to re-allocate wealth while the second relies more on the welfare state.

Is this not to be expected with a competitive global capitalist system?

The worker can be taxed easily as he cannot move his job anywhere, taxes are deducted from his paycheck and that is the end of that. There is nothing he can do about it.

The global capitalist on the other hand, has multiple bank accounts in different brokers / countries around the world. If the USA raises tax rates on corporations or taxes on capital the money is moved and invested in a different country instead. Creating a forcing affect that will basically reduce taxes on income from capital down to 0. (You can already do this easily in USA, UK, Australia with various tax concession laws, favorable treatment of capital gains, etc, this is very mathematically possible). So it can be argued that this already exists for sophisticated investors. Capital gains are tax discounted, dividends are converted into buybacks instead, and payments go to foreign countries with 0% tax rates like Cayman Islands or wherever. This means even if you can be taxed in your own country, you can just buy 100% stocks, plus leverage some amount into put options and basically pay for your own tax to be arbitraged away to the Cayman Islands for a small fee. (E.g lets say that your tax rate is 40%, Cayman Island is 0%. Investing all of your money into stocks that pay no dividend and only do buybacks, and buying long term capital gains puts instead of bonds for protection, gets your effective tax rate approx down to 0% like the Cayman Islands via arbitrage with them).

If you do all of this right, currently literally the only taxes you pay when earning capital income (in pretty much any western country) are company taxes on the equity you own, some tariffs, and some consumption taxes.

Net of the benefits your companies get (roads, infrastructure, legal system, etc), it is easy to see how this can actually be a net benefit for the capitalist, and a net loss for the average worker.

I could go into a lot more detail, but suffice to say that if you don’t understand how to make money from global capital, those that do will pull very far away from you in relative terms of wealth.

Yes, the mechanisms you list would contribute to negative redistribution. Here’s what was surprising: simple multiplicative growth for wealth is a reasonable null model (it’s the null model for all of finance), and in that model relative wealth is unstable. We started out with the belief that this model had to be corrected because surely the real system is more stable than the null model — we still have some form of democracy. We thought the relative-wealth distribution is currently getting more unequal, moving from one stable state to a less equal but still stable one. So we fitted a correction term. But it turned out that had to be negative (at least recently) because actually the system is even more unstable than the null model. It looks like we’re not moving from one stable state to another more unequal one; currently it looks like we’re blowing up.

Is this not to be expected with a competitive global capitalist system?

The worker can be taxed easily as he cannot move his job anywhere, taxes are deducted from his paycheck and that is the end of that. There is nothing he can do about it.

The global capitalist on the other hand, has multiple bank accounts in different brokers / countries around the world. If the USA raises tax rates on corporations or taxes on capital the money is moved and invested in a different country instead. Creating a forcing affect that will basically reduce taxes on income from capital down to 0. (You can already do this easily in USA, UK, Australia with various tax concession laws, favorable treatment of capital gains, etc, this is very mathematically possible). So it can be argued that this already exists for sophisticated investors. Capital gains are tax discounted, dividends are converted into buybacks instead, and payments go to foreign countries with 0% tax rates like Cayman Islands or wherever. This means even if you can be taxed in your own country, you can just buy 100% stocks, plus leverage some amount into put options and basically pay for your own tax to be arbitraged away to the Cayman Islands for a small fee. (E.g lets say that your tax rate is 40%, Cayman Island is 0%. Investing all of your money into stocks that pay no dividend and only do buybacks, and buying long term capital gains puts instead of bonds for protection, gets your effective tax rate approx down to 0% like the Cayman Islands via arbitrage with them).

If you do all of this right, currently literally the only taxes you pay when earning capital income (in pretty much any western country) are company taxes on the equity you own, some tariffs, and some consumption taxes.

Net of the benefits your companies get (roads, infrastructure, legal system, etc), it is easy to see how this can actually be a net benefit for the capitalist, and a net loss for the average worker.

I could go into a lot more detail, but suffice to say that if you don’t understand how to make money from global capital, those that do will pull very far away from you in relative terms of wealth.

Yes, the mechanisms you list would contribute to negative redistribution. Here’s what was surprising: simple multiplicative growth for wealth is a reasonable null model (it’s the null model for all of finance), and in that model relative wealth is unstable. We started out with the belief that this model had to be corrected because surely the real system is more stable than the null model — we still have some form of democracy. We thought the relative-wealth distribution is currently getting more unequal, moving from one stable state to a less equal but still stable one. So we fitted a correction term. But it turned out that had to be negative (at least recently) because actually the system is even more unstable than the null model. It looks like we’re not moving from one stable state to another more unequal one; currently it looks like we’re blowing up.

Wonderful post. Thank you. However, I’m a little disappointed by the last part of your response to Scott Thomas:

“I should also say that this is not a value judgement, it just lays out the naked mechanics. We may want to concentrate wealth and power in the hands of a small elite, corresponding to \tau<0 (that's seems to be what we're doing at the moment). Royalists have argued that that’s a good thing, and feudal societies are organized that way. At the other extreme communists would argue that \tau \to \infty is a good thing — like in feudalism, private property doesn’t strictly exist in communism. Capitalist democrats tend to be somewhere in the middle, they might want \tau \approx 2\% p.a., something small but positive. What value of \tau a society aims for is a political choice. In our work we’re just helping to measure it so that people can have an informed debate about the the choices we want to make as a society."

The happy neutrality of the scientific man should not extend over everything. Current levels of wealth and socioeconomic inequality have life or death consequences, and the political choices affecting these levels are rarely made by society at large.

Wonderful post. Thank you. However, I’m a little disappointed by the last part of your response to Scott Thomas:

“I should also say that this is not a value judgement, it just lays out the naked mechanics. We may want to concentrate wealth and power in the hands of a small elite, corresponding to \tau<0 (that's seems to be what we're doing at the moment). Royalists have argued that that’s a good thing, and feudal societies are organized that way. At the other extreme communists would argue that \tau \to \infty is a good thing — like in feudalism, private property doesn’t strictly exist in communism. Capitalist democrats tend to be somewhere in the middle, they might want \tau \approx 2\% p.a., something small but positive. What value of \tau a society aims for is a political choice. In our work we’re just helping to measure it so that people can have an informed debate about the the choices we want to make as a society."

The happy neutrality of the scientific man should not extend over everything. Current levels of wealth and socioeconomic inequality have life or death consequences, and the political choices affecting these levels are rarely made by society at large.

On political reasons for changes in tau: https://web.stanford.edu/group/scheve-research/cgi-bin/wordpress//srv/htdocs/wp-content/uploads/2013/08/ScheveStasavage_IO_2010.pdf

Inequality measures correlate with slower growth:

http://www.oecd.org/social/Focus-Inequality-and-Growth-2014.pdf

Growth is even more depressed where there is low equality and low credit availability: https://dash.harvard.edu/bitstream/handle/1/12502063/Inequality%20and%20Economic%20Growth%20-%20The%20Perspective%20of%20the%20New%20Growth%20Theories.pdf?sequence=1

On political reasons for changes in tau: https://web.stanford.edu/group/scheve-research/cgi-bin/wordpress//srv/htdocs/wp-content/uploads/2013/08/ScheveStasavage_IO_2010.pdf

Inequality measures correlate with slower growth:

http://www.oecd.org/social/Focus-Inequality-and-Growth-2014.pdf

Growth is even more depressed where there is low equality and low credit availability: https://dash.harvard.edu/bitstream/handle/1/12502063/Inequality%20and%20Economic%20Growth%20-%20The%20Perspective%20of%20the%20New%20Growth%20Theories.pdf?sequence=1

Pingback: Democratic domestic product – Ergodicity Economics

Pingback: Democratic domestic product – Ergodicity Economics

As I see this GBM model can be used for the stock market but I don’t think it is useable for real economy. First of all what is x? It is written that wealth, but wealth we can’t really measure in absolute values. We usually use money that purpose, which can measure wealth just in relative terms. Let’s say we have fix money supply. How we measure economic grow in this case? If the number of goods and services increases then prices are falling because same amount of people are chasing more products. Therefore, economic growth naturally deflationary and economic recession is naturally inflationary if the amount of money in circulation is fixed. So I guess that in GBM is basically the increment of money supply, which doesn’t necessary have connection with wealth.

The σdW term tells me that in your model every person is gambling with his money or investing it in stock market and no one is saving. This is popular just in times, when inflation (=money supply increment) is too large and there is no incentives to save money. In such an environment taxing everyone can reduce inequality increment of course but doesn’t solve the problem.

The only way to solve the main problem is to fix the money supply and taking very large obstacles to money creation. In case of sound money people instead of investing, they will just save their money. This can decrease inequality, hence, you can safely preserve your wealth. Furthermore if money is a good store of value (SOV) then no one will use stock/bonds/real estate as SOV and finally houses will have reasonable prices, affordable for poor people too. Financial bubbles/rent seekers/black swan events will disappear. So what I want to say with this is that sound money makes your model invalid due to the different incentive structure in the economy.

You could argue that if savings increase then that amount of money will not contribute to the economy. That is misleading because the amount of goods and services will not change, savings just will increase money value and poor people can afford more to buy for themselves. Rich people/investors will have lower profit margin due to lower prices. Exactly that happened between 1865-1903 in the USA: purchasing power of people’s salary constantly increased while there was a deflationary environment. Deflationary simply because economy was growing (more goods and services was made) more rapidly than the money supply.

Okay, we cant make from the dollar sound money due to the huge debt spiral we are living in. A new money have to be used, in which no one is in dept. I think you know what kind of money I am talking about.

What do you think about my thoughts?

The Reallocation of Geometric Brownian Motion as a test against reality is mathematical genius and simplicity. I think it will be superior to Monte Carlo Simulation and Martingale. The challenge in Reality is the constant introduction of new information. Stopping Information is the economists equivalent of physicists creating a perfect vacuum. David Epstein and Malcolm Gladwell have two interesting discussion, on 42 Analytics, regarding “our distortion” due to precocity, the advantages of being first and closed skills. It benefits the entity needing measurements but limits the actual participants. The inverse intuition is less measurable skills create opportunities for outliers of outliers. This follows the concept of disadvantages which create advantages.

Thank you for your work.

The Reallocation of Geometric Brownian Motion as a test against reality is mathematical genius and simplicity. I think it will be superior to Monte Carlo Simulation and Martingale. The challenge in Reality is the constant introduction of new information. Stopping Information is the economists equivalent of physicists creating a perfect vacuum. David Epstein and Malcolm Gladwell have two interesting discussion, on 42 Analytics, regarding “our distortion” due to precocity, the advantages of being first and closed skills. It benefits the entity needing measurements but limits the actual participants. The inverse intuition is less measurable skills create opportunities for outliers of outliers. This follows the concept of disadvantages which create advantages.

Thank you for your work.

Five years have past since this post was created and the forecasts herein are quite startling given inflation and internet rate increases. One gotcha though: the post’s images no longer load and I am missing the illustrations: please fix? Thank you for sharing this great idea!

Many thanks for your comment. I agree, over the last few years this has become an even more useful way to think. I’ll look into the issue with the images. You’re right, something isn’t working.

Pingback: Čo má spoločné polarizácia a miznúca stredná trieda? - OPolitike

Pingback: Literaturliste – Wohlstand für Alle

Pingback: The incorrect coin toss – TOP HACKER™

Pingback: Ungleichheit in Praxis und Theorie – Wohlstand für Alle