A central puzzle in evolutionary biology is that of spontaneous altruism. When two creatures interact, why might one sacrifice something of value in order to help the other? Why, if I’m rich, might I want to help the poor? In one view of the problem, there’s no good reason for it. By giving, I become poorer. Why would I want that? Naturally, there’s another view — one which takes advantage of the ergodicity concept — which says it’s not so much about zero-sum giving and receiving but rather about behaving in a way that benefits all in the long run. As Khalil Gibran put it, “They give that they may live, for to withhold is to perish.”

Ergodicity, we all know, is a formal mathematical concept which applies to mathematical models. In order to think about cooperation using the ergodicity concept we therefore have to write down a formal model where cooperation may or may not take place.

Tossing a coin

Our starting point is The infamous coin toss I invented many years ago, and we will generalize it. If you’ve read the blog post on it, you can skip this section and go straight to “They give that they may live”.

The coin toss is a simple example of random multiplicative growth: on heads you increase your current wealth by 50%; on tails you lose 40% of it (for ergodicity economics regulars, this is a discretized form of geometric Brownian motion). This represents the situation where there’s a quantity x of some stuff. This stuff has the multiplicative property of self-reproduction, which is common to all living things: it grows and shrinks by an amount in proportion to how much of it is currently there. The growth has a systematic trend, and also a lot of randomness. Examples of real systems with such growth include the biomass of bacteria in a sugar-filled Petri dish, or dollar-wealth in an investment account, or the population of rabbits in a field.

The coin toss has become a go-to model for explaining ergodicity and ergodicity-breaking. In stochastic processes, ergodicity expresses a type of stationarity. It implies that the expected value of a randomly changing quantity is the same as the time average of that quantity. In the coin toss, ergodicity is broken. The expected value after one round of playing is 5% more wealth (of course: there’s an equal chance of 50% up and 40% down). Since the rules of the game don’t change, expected wealth grows exponentially at 5% per round for all eternity. This suggests that it’s a game worth playing, but the ergodicity problem tells us that what happens with certainty to the expected value may not be what happens with certainty to individual wealth over time, and the coin toss is a case in point.

Over time, an individual playing the game experiences 50% gains and 40% losses in sequence, and in the long run, it will see just as many ups as downs (because the coin is fair). The result of a 50% up followed by a 40% down is not two 5% gains but a 10% loss, going from $100, say, first to $150 (the 50% up) and then down to $90 (the 40% down). The way the mathematics works out, we thus have the curious situation where the expected value of our wealth increases by 5% per round, but over time our particular personal wealth is guaranteed to decrease by about 5% per round (10% every 2 rounds).

This innocuous-looking gamble is a powerful tool, a window affording us a rather different view of economics, ecology, evolution, and complexity science. Hence all the excitement about it. To get an idea of how it behaves, choose how many rounds of the gamble you want to see and hit “Simulate” in the app below. The green straight line is the analytical result for what happens in the long run to an individual player; the red straight line is the expected value, and the wriggly random blue line is what happened to your particular wealth in this simulation. Simulate as often as you like to get an idea for how variable the results are.

“They give that they may live”

But in this blog post we are going one step further: it’s not about a lonesome coin but about cooperation. This coin toss is taunting us — it has that wonderful expected value, increasing exponentially, and yet when we play it, we’re bound to lose. Isn’t there some trick we can apply? Some way of harvesting something of those great expectations, carrying over the promise from the statistical ensemble into the individual trajectory?

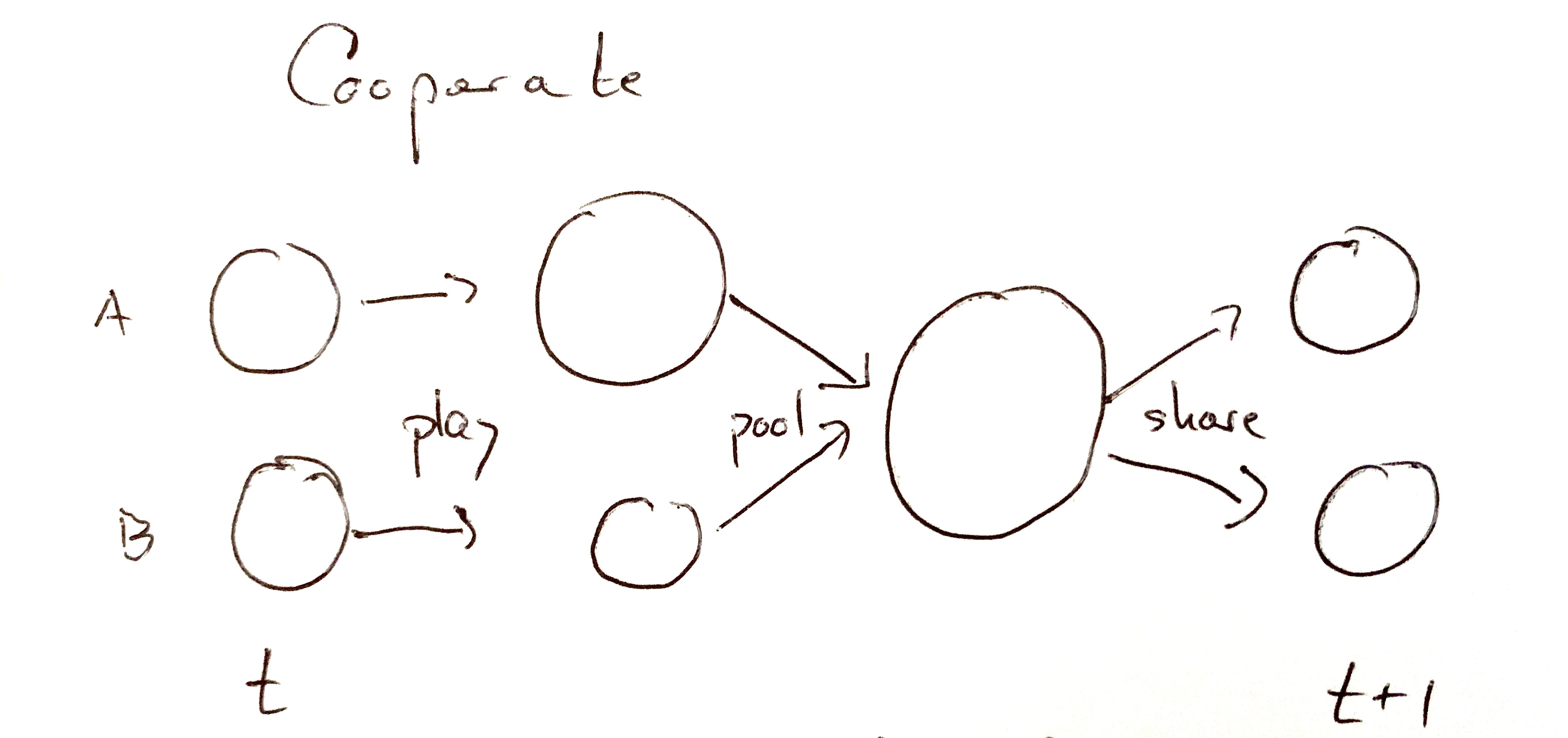

The answer is yes — and that’s one reason why ergodicity economics has become such a hot topic. There’s a very simple cooperation protocol which allows us to benefit from the coin toss. Here it is: find a partner, independently play one round each, then pool your wealth and split it evenly. Then play the next round independently, as illustrated in the figure below.

With the parameters of the gamble, pairing up in this way leads to a time-average growth rate of the wealth of the cooperating pair of -0.2% per round, compared to -5% per round for the individual player — the cooperators outperform the non-cooperators exponentially and almost break even. With one extra cooperator applying the same protocol — play independently, pool wealth, share equally — the gambling gang moves into positive territory. The time-average growth rate of the cooperating triumvirate is +1.5% per round. In this simple game, Gibran is very literally — mathematically — right: the solitary entity decays, dies with certainty. A few entities who have learned to give, on the other hand, may live.

Try it out by setting the number of cooperators to something bigger than one in the app below.

The cooperating gamblers are not doing anything new, in a sense. They’re still just gambling, they haven’t developed any special skills, they can’t predict how the coin will land. All they’ve learned is to share, and just that allows them exponentially to outperform their non-cooperating peers (or former selves).

We can keep growing the group, and in the limit of infinitely many cooperators, wealth grows at the growth rate of the expected value.

Naturally, this is quite a change in perspective for researchers who are used to optimizing expected wealth (that’s most economists, for instance). Such researchers see no value in cooperation unless new function emerges from the interaction. I can lift you up on my shoulders, and together we’re tall enough to reach an apple on a tree. That sort of thing is understood, where my shoulders acquire the new function of lifting someone up, which they cannot have while I’m alone. But the value of simply agreeing to share my apples with you is not appreciated.

Here is the reason why economics undervalues cooperation, and it’s oddly convoluted so I recommend reading the next two sentences carefully. By focusing on expected value, mainstream economics focuses on an object which grows as fast as the wealth of an infinite cooperative. Adding cooperation in this situation, where it is inappropriately assumed that perfect cooperation already exists, naturally seems pointless. Hence the impression of cold-heartedness we get from mainstream economic theory? I think so. I think this is one important reason, at least.

For full details, including the effect of differences in skills and of correlations among coin tosses of individual gamblers, read our paper in the Royal Society’s Philosophical Transactions (open access). Using time-average growth rates as the single criterion, there are limits for who should join, and who should be accepted into, a cooperating group. But the limits look different from what linear expected-value thinking suggests. The most skilled can still do better by joining a less skilled collective, and we see mathematically how important it is to maintain diversity and avoid loss of identity in a cooperating group. Lorenzo Fant et al. show in their stability analysis that cooperation can be worth it even if your partner is less cooperative than you, published in Physical Review E (free version here).

We are beginning to relate the mathematics to real social observations. For instance, Athena Aktipis and her coworkers have studied attitudes and moral codes concerning cooperation in different societies, for instance among Maasai pastoralists in East Africa. Their work indicates that where survival is key, more generous systems of mutual aid emerge. Generosity may be thought of as a spectrum reaching from the individual coin toss, where no aid is ever received or provided, to cooperative coin tossing where “aid” is provided at every step whether it’s needed or not. In between lie different forms, where records may be kept to ensure future repayment of aid, or where the severity of need determines the degree of aid provided, with no expectation of repayment.

The coin toss says: where unintended consequences can be avoided, the more sharing takes place the faster we will make progress. The optimal level of cooperation appears not as the minimum required to avoid disaster. It is instead the maximum we can get away with without triggering unintended consequences.

_________________________________________________________________________________________________

Curious about Ergodicity Economics?

Join our mailing list.

Seriously curious?

Get the textbook.

Here is my very much related post about stock diversification:

https://outcastbeta.com/diversification-is-a-negative-price-lunch/

In the world of ensemble averages stock diversification is famously ”a free lunch”.

In the world of time averages diversification is not only free, but negative price lunch.

Read your thesis with interest.

“To maintain a

constant wealth ratio, required level of diversification for a long-term risk neutral investor is approximately directly proportional to investment time horizon length.”

This turns out to be ALMOST true.

Upon (very) large scale simulations, it turns out that there is a critical regime followed by a phase transition (regardless of the type, extent, diversification, instrument, etc.) AFTER which point (“investment horizon”) your – above – contention stands and can be closely estimated. (Not an easy task to ascertain but the results are universal.)

Good work!

Your work is amazing!

Pingback: Pooling and Sharing of wealth manufacture each person’s wealth develop sooner – TOP Show HN

Simple and brilliant. Thank you for sharing.

You conclude “It is instead the maximum we can get away with without triggering unintended consequences.”

What do you refer to when you use the phrase “unintended consequences” in this context?

Thank you, Clarence, that’s a very good question, and I could have written a lot more about it.

In essence, the argument I outline in the post is an argument in favor of ‘cooperation’ (or sharing of resources). It’s not a comprehensive review of all good arguments for and against sharing resources. The reason I wrote it is that this argument is not generally understood and appreciated, whereas many good arguments against `cooperation’ are now part of our cultural knowledge.

But you were asking about examples. For instance, fully pooling and sharing your wealth removes an important incentive for wealth creation: you may want to be personally rich, richer than your neighbor. You may want to be rewarded for making more of an effort. Those incentives go away.

Maintaining mechanisms of pooling and sharing usually comes with a cost. If that cost becomes too large, then it may be a good time to dial down the sharing.

In the context of the game, there’s another effect: the benefit described here is one of diversification. But cooperation can lead to loss of diversity, and that can destroy this particular benefit.

The extreme bad case of cooperation is totalitarianism, where individuals lose their individuality and become tools of a higher-order structure, such as a state-gone-wrong.

So on long time scales, we tend to see a see-sawing between too much centralization (cooperation) and too little, and different parts of a society or economy can be on different sides of the cooperation optimum. There isn’t a simple “individualism good, collectivism bad” message or the other way around — too much collectivism eventually triggers bad consequences.

Pingback: Pooling and Sharing of wealth makes everyone's wealth grow faster by max_ - HackTech

There are some great corollaries here with some aspects of space colonization and the Drake equation.

Pooling benefits and sharing risks are common themes for expansion and survival.

Wonder what happens when it is added as a weighting mechanism…

Good work!

As for the … “There isn’t a simple “individualism good, collectivism bad” message or the other way around — too much collectivism eventually triggers bad consequences.”

… that is true. Simple it is not!

However, large scale simulations (1B row clean financial time series data) yields stable (universal?) results with (at least) one critical point and consequent phase transition into a stable regime – in all scenarios – with regard to the transition point (i.e, “investment horizon”)

I like the insight and point well made. Always like it when the math matches reality.

There would exist an optimal size for cooperation that perhaps under positive expected value regimes.

My question is does that size increase if the expected value goes negative and the goal is just surviving as long as possible.

I’d suggest that environments expected value change much faster than cultural social contract.

Hello, Thank You for your great work.

With all due respect, I’d like to point out a potential mistake in the calculation mentioned in the article. Isn’t there a miscalculation regarding the assertion that one’s wealth decreases by 10% every two rounds when flipping a coin individually?

If you are to calculate the expected value for two rounds, you must consider not only the scenario where the coin lands heads and tails once each, but also when it lands on the same side consecutively in those two rounds. In that case, the expected value over two rounds (assuming a starting wealth of 1) would be E = 1/4 * 1.5^2 + 2 * 1/4 * 1.5*0.6 + 1/4 * 0.6^2 = 1.1025. Naturally, this value is equivalent to squaring the expected value of 1.05 over one round.

Indeed, when you simulate individually, the expected value appears to decrease quickly, and wealth diminishes. However, this is because in almost all scenarios, wealth decreases, but there’s a small probability that wealth significantly increases, giving an overall expected value greater than 1.

The trick in this theory lies in the idea that the few individuals who experience a significant increase in wealth, by chance, distribute it among the majority who lost wealth. This distribution results in a steady increase in overall wealth. It’s not that the expected value changes when flipping coins individually versus in a group.

Hi Takuya,

What you say is correct, except that nothing different is asserted in the blog post. The key point is that we should _not_ focus (nor compute) expected value when assessing a gamble as an individual player.

This is because of the physical meaning of the expected value: it is the average over an infinite ensemble of players. That average, indeed, is pulled up by the rare very wealthy players, resulting in an exponentially increasing expected value, growth in 5% per round.

But the average over an infinite ensemble of players is not relevant to the individual player (unless there’s cooperation etc).

For the individual, what happens with probability 1 in the long run is precisely a decay at the time-average growth rate (not an increase at the growth rate of the expected value). The time-average growth rate is precisely that loss at 10% per two rounds, the rare exceptionally wealth trajectories notwithstanding.

The increasing expected value in the face of a decreasing time average is precisely an example of ergodicity breaking. Ergodicity is the property that expected value and time average are identical, which is evidently not the case for the coin toss.